The new tax bill signed into law in 2017 has raised many questions – and concerns – among non-profit leaders. Here is a brief recap of what’s changing for 2018:

New tax brackets have gone down: Highest rate for married taxpayers filing jointly is now 37% on income of $600,000 and above, with similar changes for single taxpayers.

Standard deduction was increased to $24,000 from $12,700 for Married taxpayers filing jointly, and personal exemptions were eliminated, with similar changes for single taxpayers.

State and Local (SALT) deduction limited to $10,000.

Mortgage interest deduction was limited for new mortgages taken after December 14, 2017. Home equity loan interest is no longer deductible.

The question for most nonprofits is: Because the standard deduction was increased, and the SALT deduction was limited, how many donors who itemized their charitable deductions in the past may no longer benefit from itemizing? Will donors decide to reduce their giving? If so, what impact will this have on revenue in the coming year and beyond?

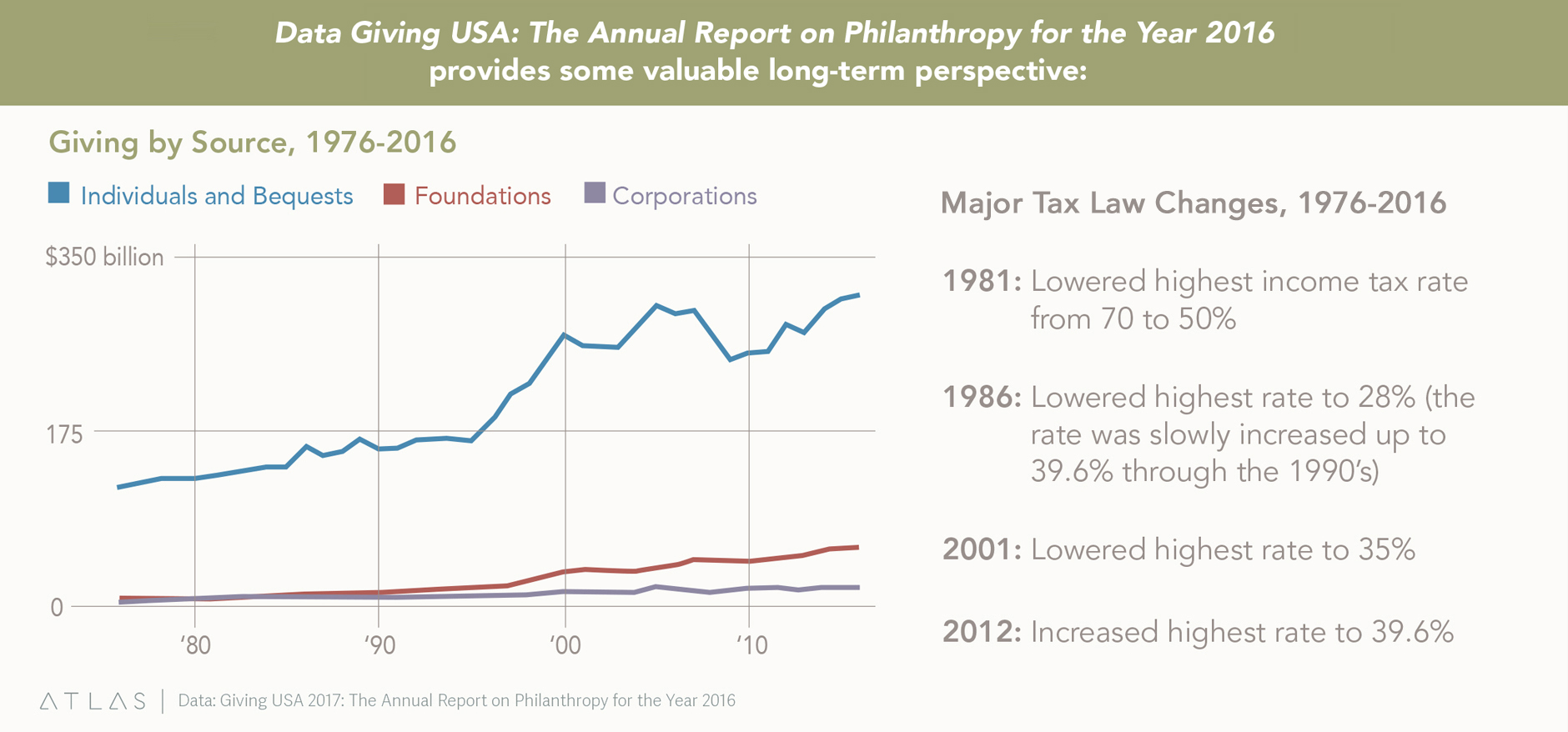

As you can see in the chart below, donations from individuals and bequests have been on an upward trend for the past 30 years, with an average increase of 1.9 percent per year. The exception was a notable decline in 2008-2009 during the Great Recession. The only other obvious decline occurred during the 2000 dot-com bubble.

There have been several tax law changes in that period, though none as directly related to the charitable deduction as the 2018 change to the standard deduction. From a historical perspective (see Major Tax Law Changes above), there doesn’t appear to be a direct correlation between tax law changes and charitable giving. Individual donors make their giving decisions due to a variety of factors. Our nation’s economic outlook plays a significant role, so the current low unemployment and high stock market valuations should indicate a positive outlook for fundraising revenue in 2018.

And we know that the single most significant factor in a donor’s giving to any individual non-profit is the donor’s connection and commitment to the mission.

Nevertheless, the tax law changes may have some impact on specific segments of the population. Anticipating those potential impacts will allow us to implement the best strategies to optimize revenue, particularly at the end of the calendar year, when tax concerns are most likely to be in the minds of donors.

Potential Impact by Donor Segment

Donors with Adjusted Gross Income (AGI) of $100,000 or less:

Minimal impact. These donors, who likely make up the bulk of the direct response file for many organizations, itemize deductions less often. However, these donors will see a small increase in their paycheck withholding if they are W-2 employees, starting in February.

Donors with AGI in the range of $100,000 to $400,000:

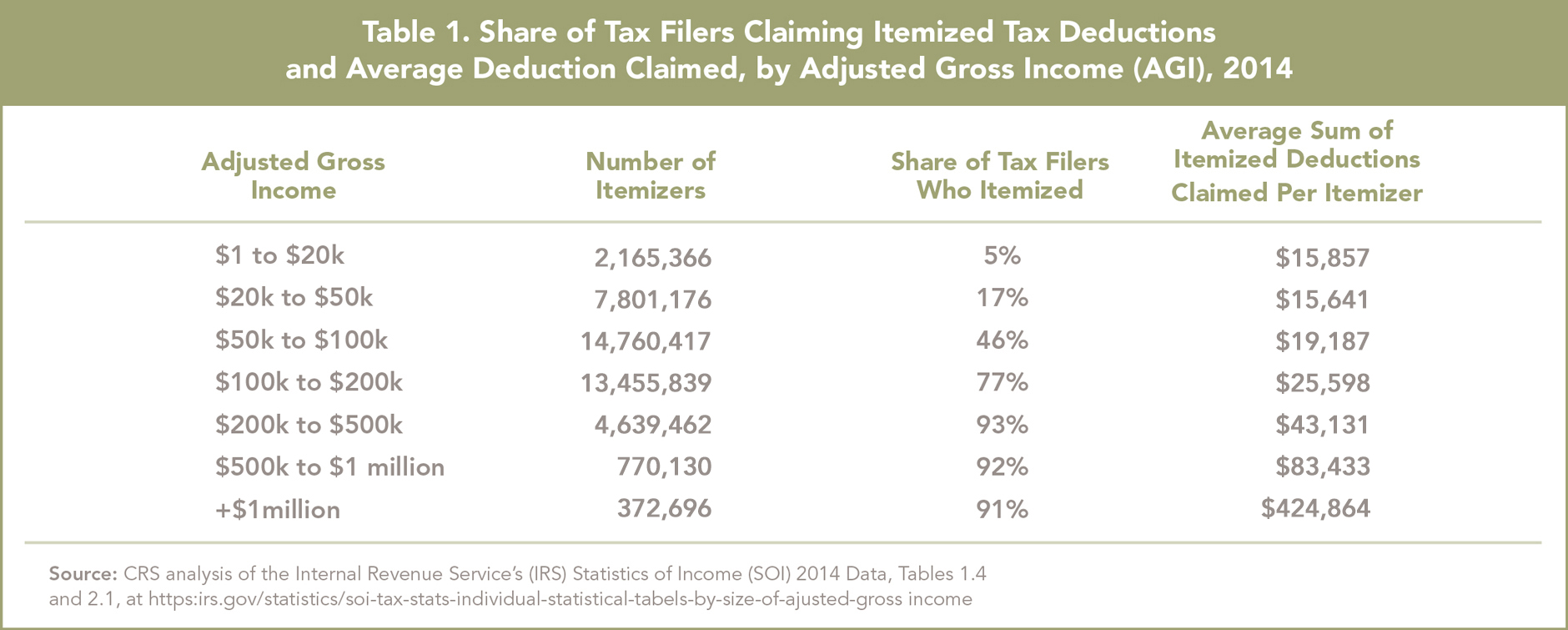

Depending on circumstances, these donors, who are likely midlevel donors giving $500-$10,000 per year for most organizations, may experience noticeable changes in their tax returns. Most donors at this income range likely itemized returns in the recent past (see chart above, 77% of filers with AGI $100;-$200k, 93% of filers with AGI $200k-$500k), and are accustomed to the benefit of the charitable deduction. It stands to reason that these donors may consider lowering their giving amount by roughly the cost of loss of the deduction (equal to the amount of their 2017 marginal tax bracket of 28%-33%).

However, these donors are likely to also experience a significant reduction in their overall federal income tax bill, due to the changes in tax rates. In particular, the shift of tax rates at the income range of $165,001-$315,000 of 28-33%, down to 24%, should provide a sizeable increase in disposable income. Ignoring for a moment the complexities of the deduction changes and the Alternative Minimum Tax (AMT), this means a donor with an Adjusted Gross Income (AGI) of $315,000 will owe $14,987 less in federal taxes in 2018 than 2017.

Every donor in this AGI range will experience slightly different results, depending on their own personal circumstances. We expect that long term these changes should offset one another for this population, but that some of these donors will reduce their giving in 2018 due to the loss of the value of the charitable deduction.

Donors with an AGI greater than $400,000:

These donors likely make up the majority of non-profit Major Gift portfolios. Most of these donors will have deductions exceeding the value of the standard deduction, such that it will be worthwhile to itemize their charitable deductions. These donors will continue to benefit from that deduction, so we do not anticipate changes in tax law to have a significant impact on their giving behavior.

Other Considerations:

Donors on fixed income, specifically donors age 65+, are of particular concern due to their prevalence in many organization's direct response files. As discussed, donors at lower income ranges are unlikely to experience a significant change. However, the value of the IRA Charitable Rollover provision as a giving tool has increased for donors age 70½ and older now that the charitable deduction is less available.

One trend we do expect to continue, or even accelerate, due to these changes, is the rise in the prevalence of the Donor Advised Fund (DAF). Because these funds allow donors to group their charitable deduction into tax years when it is most advantageous, we expect that more donors will use this tool in the future. The challenge non-profits will face will be in identifying the true donors behind the DAFs, and appropriately cultivating and stewarding those donors to cement their connection to the organizations’ mission.

Thinking Ahead: Insights for Your Year End Fundraising

THD BENCHMARKS

To stay ahead of potential revenue shortfalls, THD will proactively track and analyze year over year performance of total giving for all of our clients in the first and second quarter of 2018 analyzing key demographic indicators, including income ranges and age bands, to assess the potential impact of the new tax law changes.

If you're interested in hearing how THD's Tax Impact Benchmark can help you get a jumpstart on protecting your year-end revenue, please contact Eric Johnson.